Overhead costing is a method of setting prices for products and is often used in the catering industry. It can be carried out using a detailed step-by-step scheme or a simplified scheme.

What is the step scheme?

The step structure starts with the material costs and adds a surcharge for overhead costs to determine the cost price.

Surcharge calculation Formula

Direct costs (material costs)

Overhead surcharge

Cost price

Profit expectation

Calculated price/net sales price

Value added tax (VAT)

Inclusive price

Based on this, a profit margin is added, which defines the net sales price. The addition of VAT results in the inclusive price, i.e. the final price for the customer.

Calculation of the costing factor

Calculation of the inclusive price using a calculation factor

What is the abbreviated scheme and which ones are there?

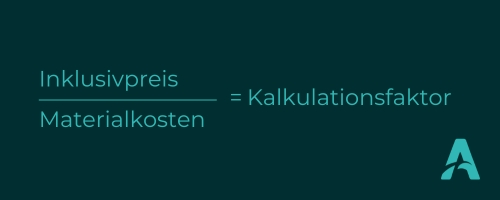

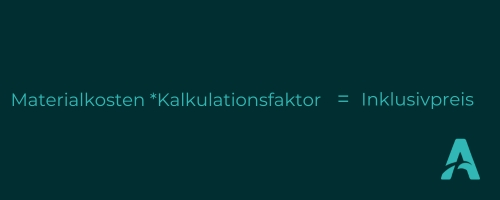

A shortened scheme uses the costing factor, which is calculated by dividing the inclusive price by the material costs. This factor, multiplied by the material costs, directly results in the inclusive price.

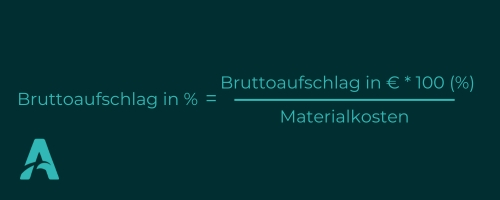

Another method is the gross mark-up, in which the mark-up in euros is calculated by subtracting the material costs from the inclusive price and converting them into a percentage. The calculation:

Gross surcharge calculation

Inclusive price

Material costs

Gross surcharge in Euro

For this purpose, the material costs plus the gross surcharge are added together to obtain the inclusive price again

Gross mark-up in %

Material costs

Gross markup

Inclusive price

Compared to the rough rule of thumb of increasing the material costs by 300-400%, the overhead calculation allows for more precise pricing.

Summary:

Surcharge calculation is a pricing method that is particularly common in the hospitality industry. The step-by-step scheme, the most common method, calculates the price by adding an overhead markup to the material costs, adding a profit markup and adding sales tax to determine the gross sales price. Alternatively, a shortened scheme can be used, which uses either the costing factor or the gross mark-up to calculate the inclusive price. These procedures enable more precise pricing than flat-rate mark-ups on material costs.